I’ve seen too many businesses tank because they picked the wrong projects to fund.

You’re probably trying to figure out which investments will actually pay off and which ones will drain your cash. The stakes are high. One bad call can set you back years.

Here’s the reality: most companies don’t fail because they lack good ideas. They fail because they put money into the wrong ones.

I’m going to show you the capital budgeting techniques that separate smart investors from the ones who just hope for the best. These are the methods I use when real money is on the line.

which capital budgeting technique is best aggr8budgeting comes down to understanding a few core approaches and knowing when to use each one. That’s what this guide covers.

You’ll learn the exact methods that help you evaluate projects, compare options, and make decisions that protect your financial health. No theory. Just what works.

By the end, you’ll know which technique fits your situation and how to apply it without second-guessing yourself.

What is Capital Budgeting and Why is it Non-Negotiable?

I remember sitting in my office three years ago when a client called me in a panic.

He’d just committed $200,000 to expand his manufacturing line. No formal analysis. No projections. Just a gut feeling that it would work out.

Six months later, he was bleeding cash and couldn’t figure out why.

That’s when I realized something. Most business owners think capital budgeting is just corporate jargon. Something only Fortune 500 companies need to worry about.

They’re wrong.

What Capital Budgeting Actually Is

Capital budgeting is how you decide which big projects or investments are worth your money.

That’s it. No fancy language needed.

You’re looking at potential projects (maybe new equipment, a building expansion, or a major tech upgrade) and figuring out which ones make sense. Which ones will actually pay off.

Think of it this way. You’ve got limited cash. You can’t fund everything. So you need a system to pick the winners and avoid the losers.

Some people say you should just trust your instincts. They argue that overanalyzing kills momentum and that successful entrepreneurs take bold risks.

But here’s what that misses. Bold risks without analysis aren’t brave. They’re just expensive mistakes waiting to happen.

Here’s why capital budgeting matters:

- You’re dealing with finite resources (your money and time don’t grow on trees)

- Every dollar you spend on Project A is a dollar you can’t spend on Project B

- Bad decisions can sink your business before you realize what happened

The real goal? Picking projects that align with where you want your business to go long term. Not just what sounds exciting today.

I use which capital budgeting technique is best Aggr8budgeting depends on your situation, but the principle stays the same. You need a formal process.

Because here’s the truth. A good capital budgeting process helps you spot financial risks before you write the check. You see the warning signs early. You avoid the disasters my client walked into.

And when you get it right? You’re not just spending money. You’re creating value. You’re building something that makes your business worth more tomorrow than it is today.

That’s why I call it non-negotiable. Skip this step and you’re gambling. Follow it and you’re investing with capital management tips aggr8budgeting that actually work.

The Three Foundational Techniques Every Planner Must Know

I remember sitting in my first budget planning meeting years ago.

The CFO asked me which project we should fund. I had spreadsheets. I had projections. But I didn’t have a real framework for making the call.

I fumbled through some half-baked reasoning about revenue potential. It was embarrassing.

That’s when I learned something important. You can’t just guess at which projects deserve funding. You need actual techniques that stand up to scrutiny. That’s when I discovered the power of Aggr8budgeting, a method that ensures your funding decisions are based on solid analysis rather than mere guesswork.

Here’s what I use now. Three methods that form the backbone of every capital decision I make.

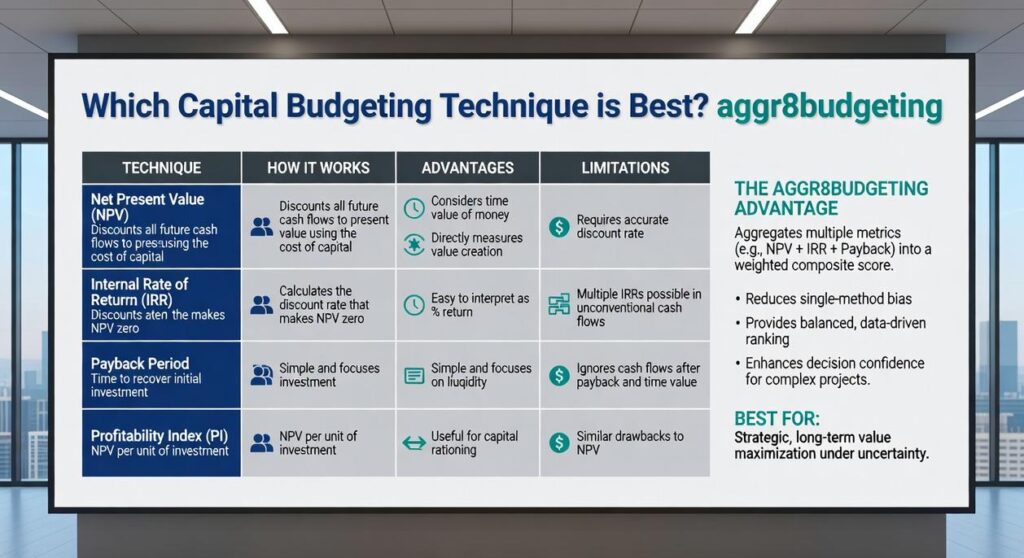

Net Present Value (NPV): The Gold Standard

NPV is the difference between what cash comes in and what goes out, adjusted for time.

You take all your future cash flows and discount them back to today’s dollars. Then you subtract your initial investment. What’s left is your NPV.

The decision rule is simple. Positive NPV means the project adds value. Negative NPV means it destroys value.

I like NPV because it gives me a dollar figure. Not a percentage or a timeframe. An actual number that shows how much richer (or poorer) a project makes you.

But here’s the catch. Your answer depends entirely on your discount rate. Change that assumption by two percentage points and suddenly a winner becomes a loser.

Internal Rate of Return (IRR)

IRR is the discount rate that makes your NPV equal zero. Think of it as the project’s breakeven return.

If your IRR is 15% and your company requires 10% returns, you’ve got a winner. The project clears your hurdle rate by five points.

Most executives love IRR because it’s a percentage. They can compare it directly to other investment opportunities or their cost of capital.

I use it all the time in presentations. It’s easier to explain than NPV.

But IRR has problems. When you’re comparing two projects that can’t both happen (we call these mutually exclusive), IRR can point you toward the wrong choice. And projects with weird cash flow patterns? IRR sometimes gives you multiple answers or none at all. I walk through this step by step in What Are Good Ideas for Business Aggr8budgeting.

Payback Period

This one’s straightforward. How long until you get your money back?

Invest $100,000 and get $25,000 back each year? Your payback period is four years.

The appeal is obvious. Shorter payback means less risk. You’re not waiting around hoping the market doesn’t change.

I use payback period when I’m worried about liquidity. If we might need that cash for something else, I want to know how long it’s tied up.

The downside? Payback period ignores everything that happens after you break even. A project that pays back in three years then generates nothing is treated the same as one that pays back in three years then prints money for a decade.

It also doesn’t account for the time value of money (though some planners use a discounted version that does).

Which One Should You Use?

People ask me this constantly.

Some say NPV is always superior because it accounts for time value and gives you a clear value metric. Others argue IRR is more intuitive for decision makers who think in percentages.

And look, they both have merit.

But here’s what I actually do. I run all three.

NPV tells me if a project creates value. IRR tells me if it beats my required return. Payback period tells me about risk and liquidity.

When I’m presenting to stakeholders, I show them which capital budgeting technique is best aggr8budgeting for their specific situation. Sometimes that’s NPV for value creation. Sometimes it’s IRR for comparison purposes. Sometimes it’s payback when cash flow timing matters most.

The real skill isn’t picking one technique. It’s knowing what each one tells you and what it doesn’t.

Because at the end of the day, you’re not just running calculations. You’re making decisions that affect real money and real people.

And that requires more than one number on a spreadsheet.

Advanced Techniques for Deeper Financial Insight

You’ve probably heard about payback period before.

It’s simple. You calculate how long it takes to get your money back. But there’s a problem with it that most people don’t talk about.

It treats a dollar today the same as a dollar five years from now. And that’s just not how money works.

Discounted Payback Period

This is where discounted payback period comes in.

Think of it as the smarter cousin of regular payback period. Instead of just counting raw cash flows, you discount them back to present value. So you’re actually accounting for the time value of money.

Here’s what that means in practice. Let’s say two projects both pay back in three years. Regular payback period says they’re equal. But discounted payback period might show that one takes four years when you factor in the real value of those future dollars. In the realm of project evaluation, understanding the nuances of discounted payback periods is crucial, especially when applying techniques like Capital Management Aggr8budgeting to ensure that the time value of money is accurately reflected in your financial decisions.

When should you use this?

You care about liquidity (like most businesses do) but you also want your numbers to make financial sense. It’s not perfect, but it’s way better than ignoring the time value of money completely.

Some finance folks will tell you to skip payback methods entirely and just use NPV. They say payback metrics ignore cash flows after the payback point. Fair criticism. But in the real world, companies want to know when they’ll see their money back. This version at least does it right.

Profitability Index (PI)

I call this the bang for your buck ratio.

The math is straightforward. You take the present value of all future cash flows and divide it by your initial investment. That’s it.

The decision rule is simple too.

PI greater than 1.0 means the project makes money. PI less than 1.0 means it loses money. Right at 1.0 means you break even (which is really just a slow way to lose money when you factor in opportunity cost).

But here’s where PI really shines.

When you’re doing capital management aggr8budgeting and you don’t have enough money for every good project, PI helps you rank them. You can see which projects give you the most value per dollar invested.

Look at this comparison:

| Project | Initial Investment | PV of Cash Flows | PI | Ranking |

|---|---|---|---|---|

| ——— | ——————- | —————— | —– | ——— |

| Project A | $100,000 | $150,000 | 1.50 | 1st |

| Project B | $200,000 | $280,000 | 1.40 | 2nd |

| Project C | $150,000 | $180,000 | 1.20 | 3rd |

Project B has the highest total return. But Project A has the best PI. If you only have $100,000 to invest, you know which capital budgeting technique is best aggr8budgeting would point you toward Project A.

That’s the power of PI. It shows you efficiency, not just total dollars.

How to Choose the Right Capital Budgeting Technique

Look, I’ve seen companies waste months arguing over which capital budgeting method to use.

They run the numbers five different ways and still can’t decide.

Here’s what I tell them. Start with NPV (Net Present Value). Period.

Why? Because NPV tells you the actual dollar value a project adds to your company. Not a percentage. Not a timeline. Real money.

I worked with a manufacturing firm back in 2021 that rejected a project because the IRR looked weak. Turns out, that project would’ve added $2.3 million in value. They missed it because they focused on the wrong number.

The Right Way to Use Multiple Techniques

Now, some people say you should ONLY use NPV. They argue that mixing methods creates confusion.

I disagree.

NPV should drive your decision. But IRR and Payback Period give you context you can’t ignore.

IRR shows you the return rate, which helps when you’re comparing projects of different sizes. Payback Period tells you how fast you’ll recover your cash, which matters if liquidity is tight.

Think of it this way. NPV is your main GPS. The other metrics are your rearview mirrors and blind spot monitors.

After running hundreds of project analyses, I’ve learned that which capital budgeting technique is best aggr8budgeting depends entirely on what you’re trying to accomplish.

A $50 million expansion? NPV all the way.

A quick equipment upgrade when cash is tight? You’ll want to check that Payback Period too. When considering a quick equipment upgrade during a financially tight phase, it’s wise to consult some Capital Management Tips Aggr8budgeting to ensure you’re making the most informed decision regarding your Payback Period.

The key is knowing what question you’re actually asking before you start crunching numbers.

From Analysis to Action

You now understand the key capital budgeting techniques that separate smart investors from the rest.

NPV, IRR, and Payback Period aren’t just formulas. They’re your decision-making framework.

Making investment choices without these tools is like navigating without a map. You’re exposing yourself to unnecessary financial risk and leaving money on the table.

Here’s what changes when you use these methods: Financial planning stops being guesswork. You start deploying capital where it actually generates returns. Every dollar works harder because you’ve done the math.

Which capital budgeting technique is best aggr8budgeting? Start with Net Present Value. It’s the foundation that makes everything else clearer.

Take your next potential project and run an NPV analysis on it. Use a realistic discount rate. Compare the result to your other options.

That single step will change how you think about growth.

The difference between businesses that thrive and those that struggle often comes down to this: one group measures before they move, the other hopes for the best.

You have the tools now. Use them.

Ask Vorric Yelthorne how they got into saving techniques and advice and you'll probably get a longer answer than you expected. The short version: Vorric started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Vorric worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Saving Techniques and Advice, Expense Tracking Tools, Expert Financial Insights. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Vorric operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Vorric doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Vorric's work tend to reflect that.

Ask Vorric Yelthorne how they got into saving techniques and advice and you'll probably get a longer answer than you expected. The short version: Vorric started doing it, got genuinely hooked, and at some point realized they had accumulated enough hard-won knowledge that it would be a waste not to share it. So they started writing.

What makes Vorric worth reading is that they skips the obvious stuff. Nobody needs another surface-level take on Saving Techniques and Advice, Expense Tracking Tools, Expert Financial Insights. What readers actually want is the nuance — the part that only becomes clear after you've made a few mistakes and figured out why. That's the territory Vorric operates in. The writing is direct, occasionally blunt, and always built around what's actually true rather than what sounds good in an article. They has little patience for filler, which means they's pieces tend to be denser with real information than the average post on the same subject.

Vorric doesn't write to impress anyone. They writes because they has things to say that they genuinely thinks people should hear. That motivation — basic as it sounds — produces something noticeably different from content written for clicks or word count. Readers pick up on it. The comments on Vorric's work tend to reflect that.